Insights

AI for networks, networks for AI: where is the value?

Coralie Muratet

Consultant Manager

When it comes to networks, operators primarily view AI as a driver for efficiency gains. Improvements in customer experience and reductions in carbon footprint are seen as welcome side effects of this pursuit, even though they arguably deserve to be central objectives. AI is also at the heart of future networks, which will be fully autonomous, and it is above all expected to drive a surge in connectivity demand.

But where does the greatest value lie for operators today—and what about tomorrow?

A potential value equivalent to 5% of revenues in 2024

AI is already deeply embedded in every aspect of network activities: planning, design, deployment, resource allocation, supervision, and maintenance. Field intervention, particularly costly and rarely quick to carry out, is reduced to its bare minimum thanks to AI deployed in upstream processes, and "augmented" by it.

Combined with virtualization and automation, AI could enable operators to optimize around half of their network processes1. This translates into both cost savings (CapEx and OpEx) and incremental revenue.

Let’s now turn to some concrete examples of already operational use cases:

- Smart planning of mobile network investments: a tier-1 operator uses predictive modeling to make better decisions about where to locate new mobile sites, how to increase capacity at existing sites, and how to densify coverage area by area. Over five years, for every dollar invested (CapEx), the operator saved $1.5 (CapEx/OpEx) and generated $5 in additional revenue, creating a total value of $6.5.

- Optimized operations management: China Mobile, in partnership with Nokia, has developed a generative AI solution connected to multiple knowledge bases and business tools for its 4G and 5G NOCs across three regions. This solution allows hundreds of engineers to ask questions in natural language and receive relevant answers more quickly, as well as automate data analysis and code generation. The result: $7 million in annual OpEx savings2.

- Predictive battery maintenance: a tier-1 operator uses AI to predict where and when mobile access network backup batteries are likely to fail. This reduces the frequency of technician site visits and extends average battery lifespan. The result is cost savings from avoided interventions (OpEx) and deferred battery purchases (CapEx), with the added benefit of lower carbon emissions. Operator revenues are protected and customer satisfaction improves thanks to higher service availability. The five-year NPV of this use case is close to $7 million, with an initial investment of just $200,000.

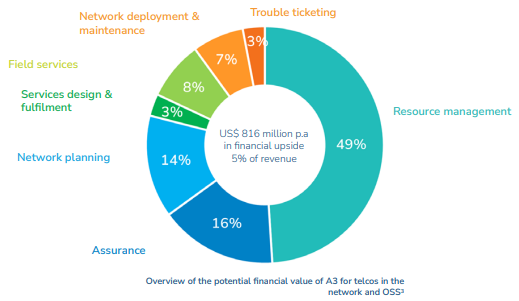

Let’s now focus on the big picture. STL Partners and Charlotte Patrick Research estimate that the value potential for a “standard operator” today is about 5% of annual revenues. A significant portion of this value comes from optimized resource management, which includes both traditional activities—such as service orchestration, energy management, and RAN management—and new AI-enabled activities like intent-based networks. (see below).

Fully autonomous networks in 4 years – at best

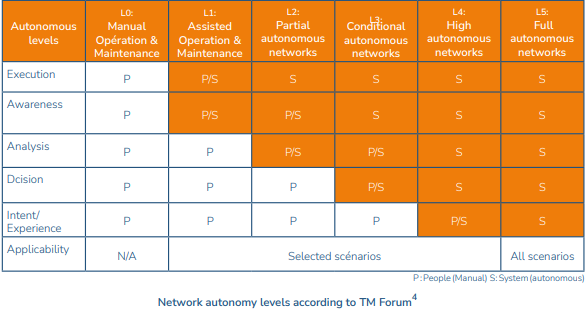

2025 should mark the transition to level 4 of network autonomy, as defined by the TM Forum. At this stage, networks will operate without human intervention in most situations, thanks to AI. No fewer than 14 operators, including China Mobile and Telefonica, plan to reach this level this year5. MasOrange, the joint venture of Orange and MASMOVIL in Spain, announced in May that it had reached it: a Europe’s première. Multiple announcements at Mobile World Congress 2025 about “AI-RAN”—the optimization of RAN resources and operations using AI—also reflect this trend.

However, full network autonomy is not expected for at least another four years, according to TM Forum. At that point, networks will be able to handle all situations, even the most complex and unpredictable, without any human supervision. Intent-based networks, leveraging generative AI, will become more prominent: network administrators will communicate high-level objectives (intentions) in natural language to multiple AI agents, which will collaborate to determine and autonomously execute the best sequence of actions to achieve those goals.

Few analysts are currently willing to estimate the value of these multi-agent systems, which are at the heart of level 4 and 5 autonomous networks, given the sensitivity and long-term nature of the topic. Among them, STL Partners cautiously suggests that these systems will account for only 30% of the total value of autonomous networks, implying that the remaining 70% has already been realized with levels 1 to 36.

AI-driven traffic explosion

Reflecting this trend, AI is expected to account for two-thirds of telecom network traffic by 2030, with total traffic potentially increasing fivefold over the same period. Operators will inevitably need to upgrade their networks. The question remains whether they will be able to monetize this new traffic appropriately and reconcile its growth with the goal of achieving net-zero carbon emissions7.

At the same time, innovative services and business models are emerging at the intersection of AI and networks, such as GPU as a Service (GPUaaS), which combines connectivity with AI service platforms open via APIs. Operators—including Orange, Swisscom, and Singtel—are gradually entering this promising market, leveraging partners or their own data centers located close to enterprise clients. This democratizes access to GPUs and meets growing demand for sovereign AI infrastructure, while improving customer experience by enabling AI model inference close to the point of use. Analysis Mason estimates that the GPUaaS market, already worth $4 billion in 2023, will grow at an average rate of 36% per year to reach $35 billion in 20308. In turn, McKinsey estimates the value of this emerging market for operators alone at $35–70 billion in 2030. While significant, it would take ten new markets of this scale to truly revolutionize the telecom business9.

Ironically, as operators pursue greater network efficiency through AI, the resulting surge in connectivity demand brings them back to their core business.

The horizon of fully autonomous networks, by comparison, still seems distant, and the path to get there is complex: data quality remains a challenge, and trust in AI to operate networks independently is still being built.

For several more years, there is likely to be more value in networks for AI than in AI for networks. This assumes that operators will better capitalize on their key role in the development of AI use cases than they did with streaming. One key factor could be to innovate in adapting their networks for AI, as some are already doing with GPUaaS.

1STL Partners, 2020-2024

2TM Forum, “China Mobile’s new GenAI solution leads to $7 million in OpEx savings”, 2024

3STL Partners, “Finding value from AI, analytics and automation (A3) in the telco network”, 2024. “Standard operator” definition: annual revenue of US$15.6 billion, annual EBITDA of US$8.3 billion, 31 million mobile subscribers, of which 60% are postpaid, 12 million consumer fixed subscribers, 3 million IPTV/Vocustomers and 900 large enterprise customers

4TM Forum, “Autonomous Networks Business Requirements and Framework”, version 3.0.0, 2024

5Analysis Mason, “The whole telecoms industry can learn from CSPs that are making the leap to Level 4 autonomous networking”, 2024

6STL Partners, Autonomous networks: the role of multi-agent systems, 2025

7Omdia, “Road to 2030: AI and the future of network services”, 2024

8Analysis Mason, GPU-as-service(GPUaaS): considerations for operators, 2023

9Mckinsey & Company, AI infrastructure a new growth avenur for telco operators, 2025

DATA & AI

How does Sofrecom support you ?