In the beginning, the interoperability of Mobile Money (MM) solutions only involved a small number of players: mainly MM operators such as:

- Indosat, Telkomsel and XL in Indonesia in 2012

- Airtel, Tigo and Zantel in Tanzania in 2014

- Airtel, Orange and Telma in Madagascar in 2016

As MM initiatives have multiplied, interoperability projects have gained momentum. As a result, the ecosystem continues to evolve with more and more players having different profiles and objectives.

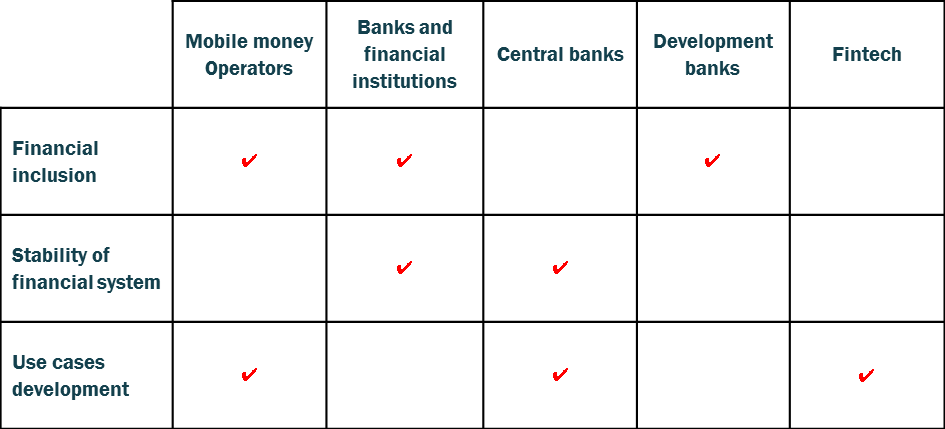

Actors with multiple profiles and motivations:

- Mobile money operators are developing new uses for their unbanked customers, for whom they are generally the main means of access to financial services (e.g. Airtel Money, Orange Money, etc.).

- Banks and financial institutions are developing new uses for their customers and are trying to rebalance the competitive space vis-à-vis MM operators (e.g. Stanbic in Ghana).

- Central banks are seeking to promote the country's financial inclusion by preserving the integrity and stability of the national financial system (e.g. Central bank of Jordan, via the JoPAAC entity).

- Development banks are developing tools that promote financial inclusion by stimulating both supply and demand (e.g. International Finance Corporation in Tanzania).

- Fintechs are developing value-added services based on mobile money. They are threatened by the interoperability and internalization of value-added services by MMPs (e.g. Interswitch in Nigeria).

The various objectives pursued by interoperability players are numerous and complementary:

Implementing interoperability requires frequent and structuring decision making

The implementation of interoperability requires preparation and an adapted response. Each component of the creation process is crucial for the success of an interoperability project. The choices made have repercussions on the viability of the interoperability project for each of the actors involved. Some choices can negatively affect some actors and favor others. It is therefore crucial to associate all the actors involved in the decision-making process in order to achieve a viable and sustainable system for all.

Thus, before embarking on a project, choices must be made that take into account the precise context of the project and the stakes of its stakeholders. These choices are related to:

The type of technical arrangement that will make the participants interoperable :

- The type of connection to be set up: bilateral connection with each participant or single connection to a central platform

- The technical standards to be respected and the levels of service, availability and security that are expected.

The business model: The success of an interoperability initiative depends largely on the ability of the parties involved to build a viable business plan. Each of its components requires decision making.

- Pricing raises many questions: is there a surcharge on interoperable transactions? Should the pricing of interoperable transactions be regulated?

- Are the transactions processed by the hub subject to interchange and do they give rise to the payment of a commission?

- Do participants have to pay a fee to be part of the interoperability arrangement?

Compensation mechanisms: participants can opt for a "pre-funded" model or a model with "settlement and compensation".

To resolve disputes, participants generally turn to dispute resolution mechanisms that must be defined in advance. This may follow the consensus or arbitration model.

Finally, particular attention must be paid to the customer journey to achieve an interoperable transaction, as it is one of the keys to adoption and success of an interoperability project. The defined paths must be clear, simple and homogeneous across all participant channels in order to provide the best possible user experience. This is a major source of user satisfaction and loyalty.

The interests of under-represented MMPs in the developing hub model

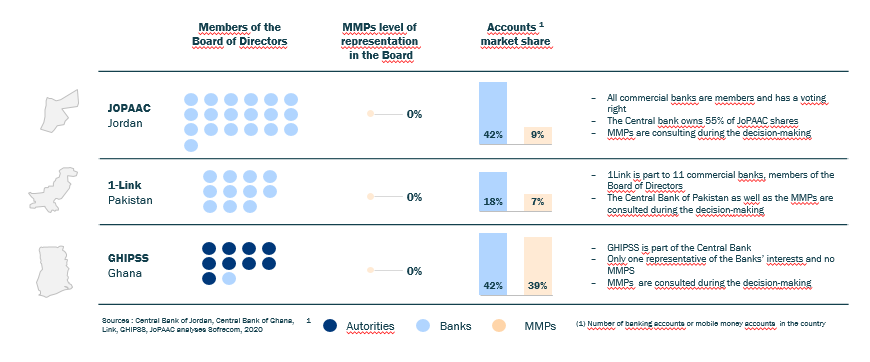

We are witnessing the emergence of the interoperability hub model, which involves players of very different natures. In this model, the participants are all connected to a central platform that hosts all the intelligence related to interoperability.

As can be seen in the table below[1], in the hub model, MMPs are integrated into governance and management systems in which it is sometimes difficult for them to be heard. They are often under-represented on the boards of interoperability hubs, which tend to give more weight and importance to banks.

MMPs and banks do not pursue the same objectives in committing to interoperability. They generally operate with different technical standards. Their business models follow different logics. As a result, the under-representation of MMPs has repercussions on the technical and business choices that are made by hub members and can ultimately negatively affect the viability of interoperability for mobile money operators.

Mobile money is the main driver of financial inclusion in emerging countries, especially among populations that are the furthest away from the banking system. Interoperability initiatives would therefore benefit from taking into account the specific features of mobile money and MMPs to meet this ambition and promote the financial inclusion of local populations. However, the first hub models do not seem to give MMPs the means to influence decision-making. The involvement of regulators is therefore essential to ensure the integration of all stakeholders. It must enable the specific characteristics of each player to be taken into account and the implementation of solutions that are favorable to everyone, and in particular for mobile money operators.

[1] GSMA – Sofrecom studies https://www.gsma.com/mobilefordevelopment/resources/tracking-the-journey-towards-mobile-money-interoperability-emerging-evidence-from-six-markets-tanzania-pakistan-madagascar-ghana-jordan-and-uganda/