Insights

Consolidation of the MVNO market: solution for a 4 operators market?

Clément Eberhardt

Wholesale consultant

Since the arrival of Free on the mobile market in 2011, France became the home for four operators (MNOs), one of which almost always endures the growth of the others: There is almost always one MNO that gives up market share so that others can grow.

This new competition has resulted in a price war which has not weakened in the last 10 years and which is leading to an erosion of operators' margins. But the mobile market, well before the arrival of Free, was already in competition, since April 20051 adding to it ARCEP's decision to require operators to host MVNOs on their networks2.

Thus, as early as 2006, Virgin Mobile, NRJ Mobile (Euro Information Telecom) and Coriolis were launched; all three were acquired by SFR in 2014, Bouygues Telecom in 2020 and Altice/SFR in 2021.

Since 2020, MVNO acquisitions have multiplied on the market, creating a new consolidation pattern: Are MVNOs that reach a critical size systematically in a position to be acquired? Will the expected consolidation on MNOs finally materialize on MVNOs?

The MVNO market in France

The MVNO market remains relatively opaque and difficult to estimate. Nevertheless, ARCEP regularly publishes observatories on the fixed and mobile markets that shed light on this market. In this case, it is the Mobile Subscribers observatory that provides the most details.

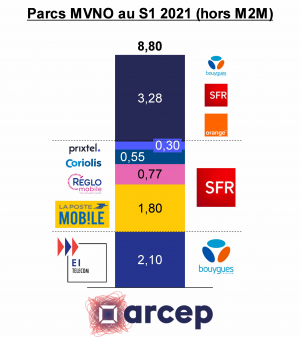

In the second quarter of 20213, ARCEP counted 6.8 million MVNO customers (VS 8.8 in June 2020) out of 75 million mobile customers excluding M2M. In 2020, EIT was the largest French MVNO with 2.1 million lines4 and La Poste Mobile was second with 1.8 million customers. Apart from these two MVNOs, only a few of them communicate on the number of customers as operators do because they are not obliged to communicate

ARCEP also communicates the list of MVNOs6 and their network provider. The majority of MVNEs are present on the Orange network, as well as corporate MVNOs. The SFR customer profile would be rather consumer-oriented, while Bouygues Telecom is more targeted towards a European Single Market. The European Single Market is represented by MVNOs that specifically address ethnic targets looking for attractive tariffs towards international diasporas.

SFR seems to be the leader in this domestic market thanks to its MVNO La Poste Mobile with the La Poste group in joint venture (1.8 million customers).

Chain buyouts and MNO strategies

In June 2020, Bouygues Telecom announced it was buying EIT for €830 million, capturing more than 2 million lines and shaking up the MVNO market. The MVNO market has not seen such a large buyout since the takeover of Virgin Mobile, the first French MVNO to reach 2 million customers, by Numéricâble-SFR in 2014.

With this acquisition, Bouygues Telecom takes on the first MVNO, present on the Orange, SFR & Bouygues Telecom networks, and addressing the B2C, B2B and Wholesale markets. This acquisition allows Bouygues Telecom to integrate EIT's customer base, thus reaching 14.5 million customers and overtaking Free and its 13.3 million customers6.

This takeover has provoked a very strong counter-attack from SFR on the MVNO market. Altice (SFR's parent company) bought Afone, Prixtel and Coriolis within a few months of each other, adding up to 1.6 million new lines.

Unlike Bouygues Telecom, Altice's strategy7 is to attack the MVNO market in order to control the wheels of the consumer market. By being the supplier of the largest consumer MVNOs (NRJ Mobile, part of EIT, leaving the MVNO market), SFR can decide on the MVNOs' retail tariffs. With this quasi-monopoly, Altice can mix its strategy of addressing customers on the French market in order to make its low-cost brand RED cohabit with MVNOs. Moreover, by using the financial advantages of joint-ventures, Altice can optimize its costs, taxes and risks that the group will share with Leclerc or La Poste for example.

For its part, Bouygues Telecom is tapping into the MVNO market to feed its MNO base and acquire EIT's expertise in the MVNE/MVNA market and the 60 MVNO customers supported by EIT before the takeover: Bouygues Telecom has invested in EIT a new Wholesale strategy by founding Bouygues Telecom Business Distribution.

Free is the only French MNO not present on the MVNO market. To date, Free has not announced any partnership with MVNOs but has recently acquired Jaguar Networks which is positioned on the Enterprise market. The MNO has just announced its will to attack the Enterprise market where it is very aggressive. Everything leads us to believe that Free could have the same attitude if it launches itself on the MVNO market.

Orange is not very active in this consolidation drive. One can imagine several reasons but the first one is the state of competition. As Orange is the leading French operator, ARCEP and the Competition Authority would strongly observe a willingness to extend. On the other hand, Orange does not have the same need as Bouygues or Free to create a skill as MVNE/MVNA.

Finally, Orange, through its positioning on the business MVNO market, does not have the same issues as SFR, which must be more responsive and aggressive8 through its consumer positioning.

Finally, we can note that the acquisition of the MVNO Transatel by the Japanese NTT in March 20199, does not intervene in a logic of consolidation of the French market but more in a perspective of acquisition of a European footprint and know-how.

What's next?

With these various takeovers, the list of French MVNOs with a critical size is considerably reduced. The remaining MVNOs are highly specialized, including:

- Business MVNOs (Sewan, Alphalink...)

- IoT MVNOs like Cubic and Truphone

- Single market MVNOs: Lycamobile, Lebara, Syma Mobile and China Telecom.

They represent about 3 million lines. For Orange and SFR, who currently lead the duopoly of the business market in France, the takeover of business MVNOs seems delicate with respect to competition law. On the other hand, Free could decide to enter the market via this approach but today no movement has been spotted.

The vertical consolidation MNO-MVNO is probably coming to an end before the long tail10 is addressed. Instead, we are seeing horizontal MVNO-MVNO consolidation. The latest one is Adista and Unyc, which have jointly announced that they are entering into exclusive negotiations, backed by Keensight Capital. In the past, Adista had already acquired Waycom and Fingerprint.

Finally, MVNOs continue to grow and acquire companies to differentiate themselves from MNOs and MVNO competition. For example, Sewan has just announced the acquisition of the cloud company Ikoula11.

The horizontal consolidation that was expected in the MNO market did not happen, but it is in the MNVO market that it is accelerating. Following a strong vertical evolution, the ball is now in the court of the MVNOs. Many of them are still aiming at external growth by integrating competitors' fleets in order to reach the critical size necessary for a vertical integration.

Definitions

MNO: Mobile Network Operator. In this article, MNO refers to the 4 French operators: Orange France, SFR, Bouygues Telecom and Free.

MVNO: Mobile Virtual Network Operator. These are operators registered with ARCEP and who use one or more MNOs to benefit from their network in order to propose offers on their behalf.

There are several types of MVNOs:

- Light MVNOs, which use all the technical resources of the MNO (radio access, core, IS, links). They benefit from the roaming agreements of the MNO that hosts them and do not pay for call terminations

- Full MVNOs that use their own network core. A full MVNO enjoys greater freedom of action and can therefore get supplies from different operators without having to create another MVNO. Unlike light MVNO, full MVNOs have to make their own roaming agreements or use those of an MNO via a sponsorship contract and pay its call termination.

- MVNEs: Mobile Virtual Network Enabler. They offer technical solutions and services enabling an MVNO to launch an activity

- MVNAs: Mobile Virtual Network Aggregator. They position themselves as intermediaries and provide expertise and connectivity.

[1] https://www.arcep.fr/actualites/les-communiques-de-presse/detail/n/lart-propose-dimposer-aux-trois-operateurs-mobiles-metropolitains-une-obligation-de-faire-droit-au.html

[2] See the box with the definitions

[3]Source ARCEP

[4] Fleet to be integrated into Bouygues Telecom's fleet following approval by the Competition Authority

[5] https://www.arcep.fr/professionnels/operateurs-des-telecommunications/liste-des-mvno.html

[6] Q2 2021 data in operator publications

[7] Sources: financial publications and press releases

[8] The consumer market is a market where offers change much more frequently and pricing is more aggressive

[9] https://www.lesechos.fr/tech-medias/hightech/telecoms-le-geant-japonais-ntt-rachete-le-francais-transatel-995170

[10] Very small market players

[11] https://www.telecompaper.com/news/sewan-strengthens-cloud-capabilities-with-acquisition-of-ikoula--1398874

Enhanced Customer Experience

Elevate customer experiences beyond expectations