The interoperability of mobile financial services is one of the essential foundations for the financial inclusion of populations, particularly in developing countries. Just like voice and SMS, it is undeniable that the development of mobile money requires opening up transactions to users who are not subscribed to the same operator. The main use case that represents one of the pillars of interoperability today is peer-to-peer (P2P) money transfer.

Successful interoperability, more than an interconnection problematic

Technical interconnection guarantees the successful implementation of an interoperability project. However, it does not guarantee user adoption. To facilitate adoption and ensure customer loyalty, it is necessary to design a customer journey centered on the user of the solution.

A quality P2P cross-net1 user experience should be as close as possible to the existing P2P on-net2,

journey, including fewer clicks and screens, understandable messages, and clearly identified options for the customer.

Sofrecom has recently conducted a study of user experience in countries where mobile money interoperability is operational. The objective was to observe the fluidity of user experience and to evaluate the capacity of adoption of the interoperability service by the people. Despite growing3, smartphone penetration in Sub-Saharan Africa, it is noteworthy that the USSD remains the preferred channel in the region.

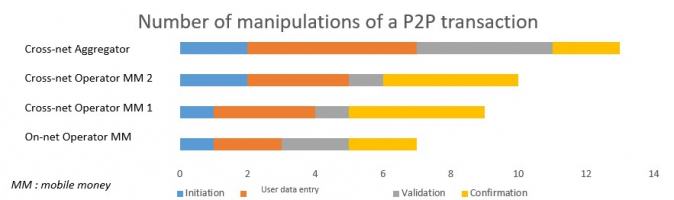

Observations in one Sub-Saharan African country show that a P2P on-net transfer takes an average of 7 steps versus an average of 9 to 13 steps for interoperable operations.

Comparison of the number of manipulations between an on-net path and the different interoperability solutions implemented – extract from Sofrecom's observation

"I prefer to go to a mobile money booth when I want to send money to someone who uses a different network to avoid the hassle of doing it myself" - Testimony of a mobile money user in Sub-Saharan Africa

Although using platforms with improved usability options compared to USSD, the aggregator applications require in our case study a longer journey. This is due to a less automated transaction routing mechanism, requiring the user to manually identify the operator of the sending and receiving accounts.

On the other hand, mobile money providers face the challenge of aligning the USSD interfaces of their on-net and cross-net transactions. The difference is that the user has to select the network to which he wants to send money. This step could be optimized through the use of dial plan prefixes when they are standardized between operators. Tools such as PathFinder4 from the GSMA can address this issue. In fact, PathFinder provides real-time access to fixed and cell phone numbers by operator, taking into account numbers’ portability.

Clear communication contributes positively to user acceptance

Communication plays a decisive role in consumer’s experience. We have observed several phenomena that can strongly hinder mobile money interoperability adoption.

The use of overly technical terms on the commercial display or SMS confirmation notifications are difficult for readers to understand and complicate the financial awareness and education exercise for field agents. In addition, the fact that several offers are marketed on the same poster does not help to identify the relevance of the service. Finally, we note that pricing information is not always standardized among the displays in the store, at the agents' offices, on the websites and the prices actually applied and visible on the USSD menu. These shortcomings create great confusion for first-time users of interoperability services.

A simplified user experience is a key requirement for scaling up mobile money interoperability

Interoperability is a relatively new service for many mobile money users. Its adoption and scaling depend on a number of factors, including the user experience.

The additional effort that a user must make to perform an operation that deviates too much from the on-net model leads to low usage or even abandonment of the service. The preferred alternatives are intermediation via an agent (direct cash-in to the recipient's account) or the use of informal services such as travel agencies.

Furthermore, in a context where there are challenges not only in terms of user financial education but also literacy, clarity of communication must be a central concern for interoperability operators.

In consequence, user-centricity appears to be crucial if we want to improve the resonance of interoperability among consumers and thus stimulate usage by the general public. For countries where interoperability is a reality, it would be wise for operators to ensure that their approach is in line with a user-centric approach.

1Transaction between 2 users subscribed to different operators

2 Transaction between 2 users subscribed to the same operator

3 Source: GSMA. In 2018, smartphone penetration in Sub-Saharan Africa was 39% and will reach 66% by 2025